Inside the PPO Stack: A Technical Guide to Dental Network Optimization

Every practice owner feels the same compression. When Dentalogic analyzed the numbers in 2022, the billed-fee trend across dentistry was running around 2.6% to 2.8% annually while reimbursement from contracted carriers crept up around 0.7% to 1.4%, and in late 2025 polling by the ADA Health Policy Institute, more than half of dentists still named insurance issues, including low reimbursement rates, among their top concerns for 2026. That gap compounds, and a practice that has participated with the same carrier for ten years without intervention is accepting a deeper discount today, in real terms, than it did the day the contract was signed.

The reason most fee conversations never get past "call the carrier and ask for an increase" is that the architecture of how a practice actually gets paid has become genuinely opaque. A patient walks in with a Guardian card. Your front desk pulls coverage. The EOB comes back three weeks later showing a fee schedule that is not your Guardian direct fee schedule, may not be one you remember signing, and may be lower than both. That outcome is the network stack working exactly as designed.

This article looks at how carriers construct reimbursement on a claim by claim basis, why the real leverage sits upstream of any individual fee schedule, and what optimization looks like when you start from the architecture instead of the line items.

The Stack: Direct, Swap, Lease, and the Lease of a Lease

A national dental carrier today does not run one network. It runs a direct network plus a set of contractual relationships that extend its reach into other rosters and other fee schedules. Four layers cover most of what a practice will encounter.

- Direct contracts. A practice signs an agreement with Aetna, MetLife, Cigna, Guardian, or a similar carrier. The carrier sets the fee schedule and pays the claim. This is where nearly every practice's contracting history started, and it is the only layer most offices actively track.

- Swaps. Two carriers agree that, in geographies where one has weaker network density, the other's directly contracted dentists become accessible to its members. In Dentalogic's 2022 mapping, Ameritas used its direct network alongside swaps with Aetna, Guardian, and Principal. Practices rarely sign anything new when a swap happens. The relationship arrives by amendment, by network bulletin, or sometimes by inference from a claim that does not look right.

- Leased networks. A separate company, often called an umbrella network, builds a roster of contracted dentists and rents that roster to carriers and TPAs that do not want to build their own. Connection Dental, DenteMax, Careington, Premier Dental Network, and Zelis (which consolidated Maverest, Stratose, HFN, and several other networks under one roof starting in 2016) are the major aggregators. A single Zelis contract can put a practice in-network with more than 40 carriers, TPAs, brokers, and self-funded employer plans, often with little notice to the practice about which plans have switched access on or off.

- Second-order access. Aggregators also build layered access among themselves, partnering with and reaching through one another's rosters. The practical effect is that a practice contracted with one umbrella can surface as in-network with a carrier it never joined, through a path invisible from its own paperwork, and frequently never knows until the EOB arrives.

Industry analysis from NetMinder found, as far back as 2016, that the average contracted dentist participated with roughly 55% of the top 15 national dental PPO networks, and nearly half were in eleven or more. A decade of consolidation later, nothing about that picture has gotten simpler. That web of relationships is the universe a carrier's claims engine is working with when it prices your claim.

How a Claim Actually Gets Priced

Here is the part that surprises practice owners the first time it is explained clearly. When a member's claim hits the carrier, the adjudication system determines which contractual path connects the rendering provider to that member's plan: direct contract, swap, leased network, lease of a lease. Carriers work through a stack order, typically the direct agreement first, then swaps, then leased networks.

One path wins, and the entire claim prices under that path's fee schedule. The EOB shows the result without showing the alternatives, so nothing on the remittance tells you which other paths existed or whether a higher-paying agreement was sitting one rung up the stack.

The ranking moves underneath you

The problem is which path wins and how that ranking changes over time. When a carrier holds multiple routes to the same provider, the deepest discount is the one it has every financial incentive to rank first, and carriers occasionally put this in writing.

When Sun Life's Dental Health Alliance opened its network to Cigna PPO members effective March 1, 2025, the notice to DHA dentists stated that the DHA fee schedule would apply to those members unless the dentist also participates in another network Cigna accesses, in which case reimbursement can shift to that other agreement. That is the stack mechanic, described by the carrier itself.

As carriers re-optimize their stacks, a practice's reimbursement gravitates toward the lowest-fee agreement it holds anywhere in the web, which is why an office can watch a book of business quietly reprice after signing nothing new.

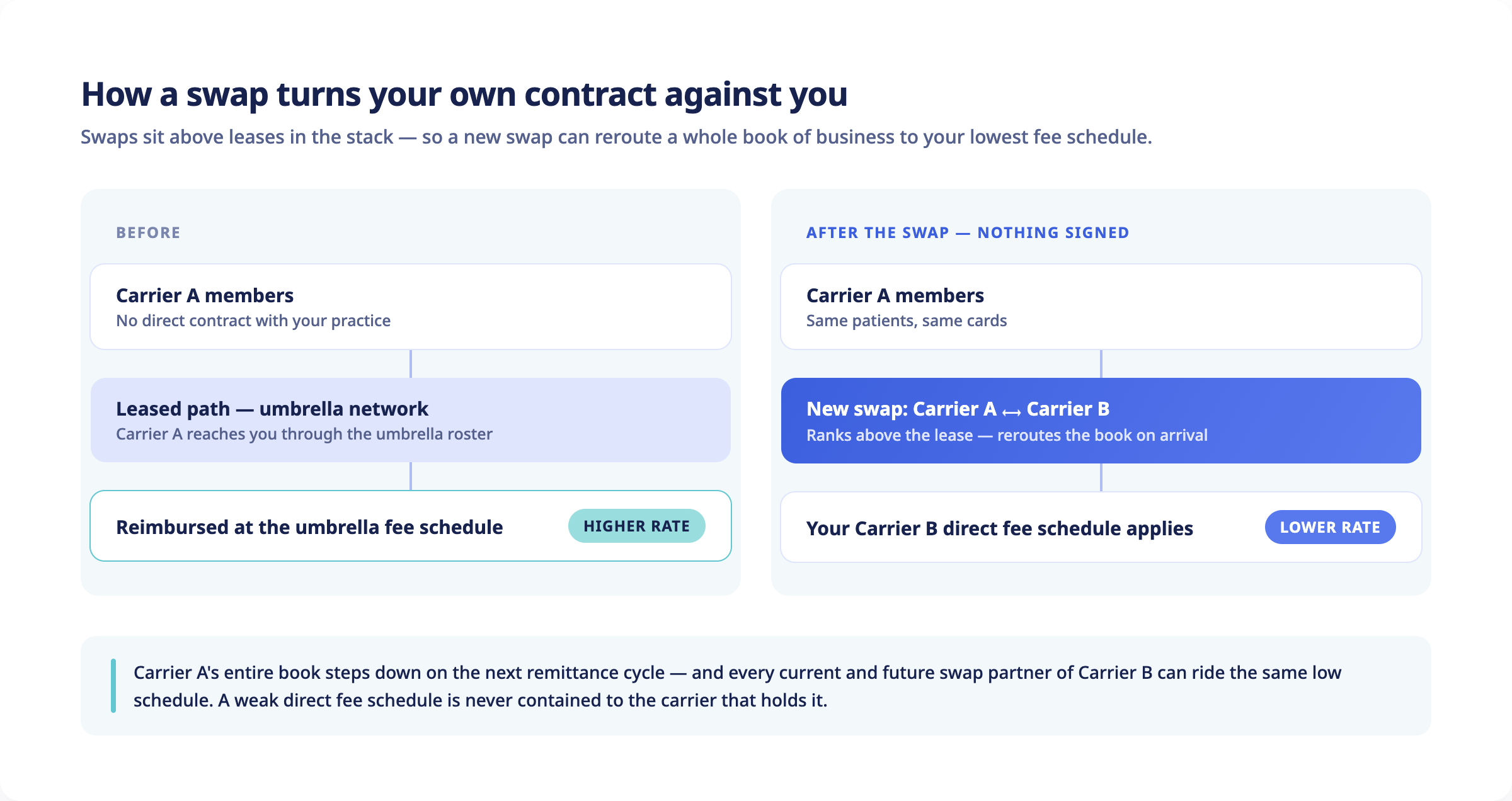

Swap exposure: when your own contract works against you

Swaps produce the sharpest version of this, because they can turn the practice's own direct contract into the instrument of a pay cut from a different carrier. Since swaps sit above leases in the stack, a carrier that has been reimbursing the practice through an umbrella relationship will reroute the moment it picks up a swap with a carrier the practice holds a direct agreement with. If that direct fee schedule is the lower number, the swap partner's entire book of business starts pricing at it, and revenue the practice had been collecting through the umbrella steps down on the next remittance cycle.

This is also why a weak direct fee schedule is never contained to the carrier that holds it. Every current and future swap partner of that carrier can ride the same schedule, which means the real cost of keeping a low direct agreement includes volume from carriers the practice has never thought about in the same breath.

The view from the EOB

The practice-side version is well documented. The ADA has described cases where a dentist treats a patient expecting full fee or a known contracted rate, and the EOB arrives priced under a leased relationship the office never connected to that carrier, with balance billing prohibited, because the plan never notified the dentist that participation had transferred through a lease.

One clarification worth making, since the marketing around this topic often gets it wrong: the per-line surprises practices see every day, meaning downgrades, bundling, alternate benefit substitutions, and disallowed codes, all occur under the single contract the carrier applied to the claim. The network selection itself happens once per claim.

The practical takeaway is that the fee schedule applied to any claim is the output of the carrier's stack, and managing individual fee schedules without managing the stack leaves the biggest variable untouched.

Why Negotiation Alone Has a Ceiling

There is a real role for direct fee negotiation. If you have not asked Cigna for an increase in five years, you should. The problem is structural. Carriers limit how frequently a practice can request an increase, and the increases they grant are designed to trail the trend in practice costs. The carrier knows what wage growth looks like and what dental supply costs are doing. They are not in the business of letting your effective discount shrink in real terms.

It gets worse. A negotiated increase only touches the direct fee schedule, so any member group that reaches the practice through a swap or a leased path never sees it. The negotiation moved one schedule in the stack while the volume routed through every other schedule stayed exactly where it was.

In a case Dentalogic published from its own client work, a practice with four direct carrier contracts went through a full negotiation cycle, received three increases, and netted $8,383 in annual impact. Optimization across the same four carriers produced $62,000. Negotiation moved individual numbers on individual contracts, while optimization changed which contracts applied to which patients in the first place.

The Dental Basket: Comparing Fee Schedules in a Single Number

Before getting to tactics, there has to be a way to compare fee schedules without going line by line across hundreds of codes. The standard tool is the Dental Basket, which weights the fifteen most frequently performed codes by specialty against a practice's actual procedure mix. For general dentists, those fifteen codes account for roughly 76.6% of total procedure volume. Periodontists, endodontists, oral surgeons, and pediatric practices have different basket compositions, but the concept holds.

Once the basket is normalized to 100%, any fee schedule reduces to a single weighted-average reimbursement number that can be compared apples to apples against any other. This is the only honest way to answer questions like "If I drop Ameritas direct and route those patients through Connection Dental instead, am I better off?" A line-by-line comparison misleads because some codes go up while others go down. The weighted basket tells you the net.

The spread matters more than most owners expect. In the Guardian analysis Dentalogic published, moving those members to the strongest network path in the carrier's stack produced a 27% lift on the weighted basket. That spread is the prize.

Optimization: Picking Your Path Into Each Carrier

The actual work of optimization is identifying, for each carrier the practice sees volume from, which contractual path produces the highest weighted basket while keeping the patient in-network. A simplified version of the process:

- Pull every fee schedule the practice has access to, direct or leased, and reduce each to a Basket number.

- For each carrier, map every swap and leased path that carrier actually uses in the practice's region, in the order the carrier applies them. This requires either carrier disclosure or empirical reconciliation against past EOBs.

- Identify which direct contracts can be terminated without losing patient access, because the patients will still be in-network through a higher-paying leased path.

- Identify which leased contracts to add, terminate, or substitute.

- Sequence the terminations and additions correctly, because some carriers have historically been slow to recognize providers under leased paths after a direct termination, sometimes leaving a multi-month credentialing gap that has to be planned around.

Dentalogic's published four-carrier case shows the shape of it. That practice joined two umbrella networks, Connection Dental and Zelis, then terminated its direct agreements with Ameritas, Guardian, and Principal. Ameritas members moved to the Connection Dental and Zelis fee schedules, Guardian members moved to the Aetna agreement, and Principal members moved to Zelis, with less credentialing to maintain and a meaningful reimbursement increase across the whole book. The patients kept the same insurance cards and never felt the change. The practice saw it on every EOB.

The same logic applies across carriers and regions, depending on which swap and umbrella relationships each carrier consumes in a given market.

The MetLife Question and Why "In-Network with Everyone" Loses

MetLife deserves its own discussion because its structure creates one of the clearest optimization case studies in the industry. PDP Plus is MetLife's flagship PPO network, while the legacy PDP fee schedule still applies to some older plans. Umbrella access to MetLife is narrower than most practices assume. Consultant reporting in recent years has described routes through companies like Careington as reaching only PDP Plus and FEDVIP plans, leaving the practice out of network with legacy PDP groups, with Connection Dental not accessing FEDVIP at all, and credentialing through those third-party paths running slow, in some reported cases approaching a year. That access map shifts, and it is worth reverifying at the time of any contemplated move.

The complication that makes this interesting is MetLife's out-of-network behavior. Plan designs vary by employer group. Some reimburse out-of-network claims at high reasonable and customary percentiles, with the 90th percentile documented on richer plan designs, and reimbursement at that level can exceed the PDP Plus contracted fee schedule for a lot of practices. Other groups use MAC-based out-of-network reimbursement, which caps payment at a maximum allowable charge and shifts the balance to the patient.

The decision to drop MetLife direct therefore depends entirely on the plan-design mix of the practice's actual MetLife patient base. A practice weighted toward 90th percentile R&C groups can often net more revenue out of network on the same volume, retaining leased access only for the sticky employer groups that need it. A practice weighted toward MAC groups cannot. This is why the analysis has to run on the practice's own EOB history rather than on a rule of thumb, and it is also why "I want to be in-network with everyone to keep my patients" is a self-inflicted wound when the same carrier pays well out of network.

What Changed in 2025 and 2026

Two developments materially affect optimization plans being built today.

The first is the arrangement between Sun Life's Dental Health Alliance and Cigna that took effect March 1, 2025. Under DHA's notice to its contracted dentists, Cigna PPO members gained in-network access to the DHA network in all states, with an opt-out window for providers who declined, and the notice was explicit that the DHA fee schedule applies to those members unless the dentist also participates in another network Cigna accesses. For a practice holding both a Cigna direct agreement and DHA participation, that language leaves an open question about which schedule each Cigna member actually reaches the practice through, and the answer should come from the practice's own EOBs rather than an assumption. Any practice holding either relationship should be modeling both paths.

The second is Aetna's Medicare Advantage restructuring. Careington began notifying Care Platinum providers that, effective September 1, 2025, Aetna would no longer access them for its Medicare Advantage plans, and nearly ninety Aetna MA plans across more than thirty states were expected to be discontinued for the 2026 plan year, most of them PPO products. Practices that historically relied on Careington as their access path to Aetna MA patients have lost that pathway, with direct Aetna PPO contracting or Connection Dental described in those notices as the remaining access points. A practice needs to know which one its actual Aetna MA patient mix routes through before renewals lock in.

These are not minor tweaks. They are the kind of network-architecture changes that should trigger a recalculation of every Cigna and Aetna patient's expected reimbursement path.

Regulation Is Catching Up, Slowly

The American Dental Association tracked 37 dental insurance reform laws passed across 18 states in 2025, following 16 laws in 9 states in 2024. The bulk of those laws address downcoding (where a carrier pays a different, cheaper procedure code than the one submitted), bundling (where multiple codes are administratively combined into a single lower-paying code), and virtual credit card opt-in provisions (where carriers were defaulting providers into VCC payments carrying per-transaction fees that state legislative analyses have put as high as 5%, a hidden additional discount on top of the contracted fee).

These reforms help, and the network-leasing laws that preceded them help more than most offices realize. States that adopted versions of the NCOIL Transparency in Dental Benefits Contracting Model Act require contracting entities to identify in writing the third parties with access to the network, to give providers at least thirty days notice before a new lease takes effect, and to allow providers to opt out of third-party access, and some versions let a provider request a copy of the contract relied on to adjudicate a claim. What no state delivers is the disclosure that would matter most: in most states the remittance itself still does not have to identify the path that priced the claim, and nothing entitles a practice to the carrier's full stack order. Network architecture remains a place where the carrier's information advantage is enormous, and the practice's leverage depends almost entirely on how thoroughly it has done its own homework.

What This Actually Looks Like Operationally

For a single-location independent practice with five to seven major carrier relationships, a serious optimization project runs through the following work:

- Pull and digitize every fee schedule the practice can access, direct or leased, including the obscure ones the office forgot it signed.

- Build a procedure-mix-weighted Basket for the specific practice rather than a generic GP basket, since pediatric, perio, and surgically heavy practices carry very different exposure to the high-spread codes.

- Map, carrier by carrier, which leased paths are actively in use in the practice's geography. Carriers rarely disclose stack order, so this usually means reconciling historical EOBs against known fee schedules until the routing reveals itself.

- Model patient-disruption risk for every contemplated termination. The worst outcome is terminating a direct contract and hitting a multi-month credentialing gap on the leased path that was supposed to catch those patients.

- Sequence terminations and additions across a six-to-twelve-month rollout, with the front desk briefed on script changes for the affected patient groups.

The published comparison frames the stakes: roughly $8,000 of annual impact from negotiation against $62,000 from optimization across the same four carriers. Erick Paul, who wrote that analysis, described the result as a common one across the more than 500 practices he has optimized over his career, with the specific strategy differing for every practice. The structural difference is that negotiation moves a single number on a single contract, while optimization changes which contracts apply to which patients.

Why This Work Goes Stale

There is a real cottage industry of PPO consultants now, and the quality varies widely. Some firms run a national-average basket comparison and call it optimization, which is closer to a sales lead than a recommendation. The work that matters is empirical, practice-specific, and rooted in actual claims data. Carrier stack orders shift, umbrella networks acquire and divest each other, and the plan-design landscape under self-funded employers is itself in flux. An analysis from 2022 is no longer accurate in 2026.

Dentalogic builds the basket from the practice's own production, reconciles it against the practice's actual EOB history, and models the optimization paths using carrier-specific stack behavior as of the current quarter. The numbers move every year, which is why PPO optimization belongs in the same rhythm as your annual fee review rather than sitting on a shelf as a one-time engagement.

If your practice has never run a serious optimization analysis, the conservative expectation is that there is meaningful money on the table, and most practices that go through it find more than they would have guessed.